Published February 21, 2026

How to Calculate Intrinsic Value (Step-by-Step)

Learn exactly how to calculate intrinsic value using a simple DCF model. A step-by-step guide for retail investors with real formulas and examples.

Marcus Chen

Senior Writer

Most retail investors never calculate intrinsic value. They check a stock's P/E ratio, see analyst price targets, and decide the market is probably right. Then they wonder why they consistently buy near the top and panic near the bottom.

The investors who actually build wealth do something different: they form an independent estimate of what a business is worth and let that anchor their decisions. This guide shows you exactly how to do that, step by step, using a Discounted Cash Flow (DCF) model—the same framework used by professional value investors.

No finance degree required. Just clear thinking and honest assumptions.

What "intrinsic value" actually means (and why price is irrelevant)

Intrinsic value is the present value of all cash a business will generate for its owners from now until the end of time. That's it. Not what the market says it's worth. Not what CNBC says. Not what the P/E multiple implies.

Price is a vote. Intrinsic value is a measurement.

The opportunity for retail investors is that Mr. Market is emotional and short-sighted. A stock can trade 40% below its intrinsic value for months simply because sentiment is poor. Your job is to exploit that gap—but only when you've done the math yourself.

The DCF model in one sentence

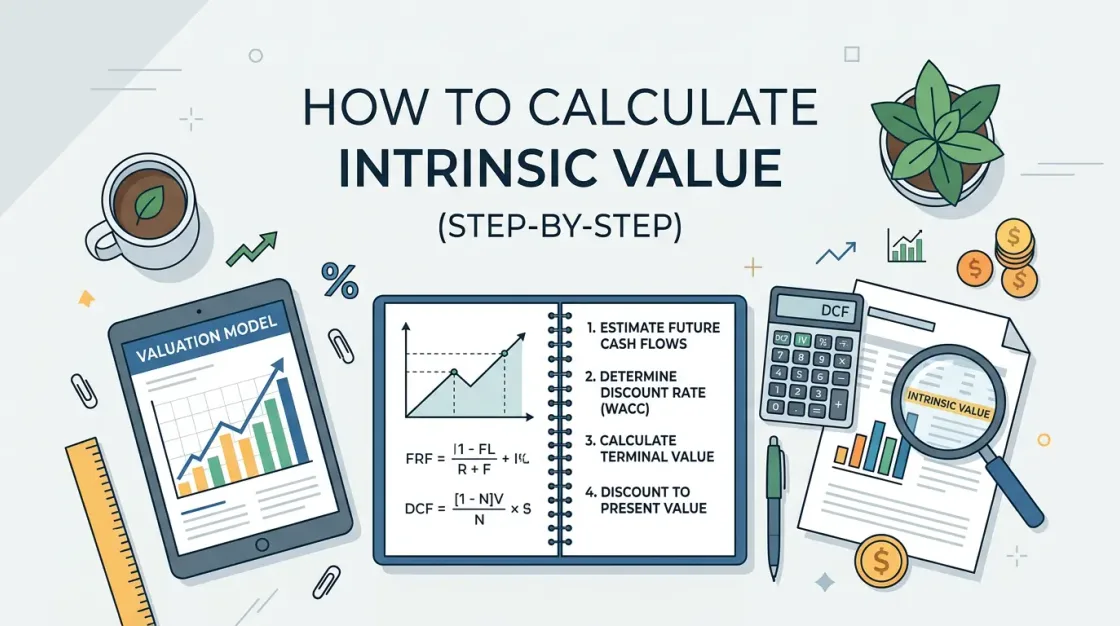

Estimate how much free cash the business will generate over the next 5–10 years, discount each year's cash flow back to today at your required rate of return, add a terminal value for everything beyond that horizon, adjust for cash and debt, then divide by shares outstanding.

The master formula:

Intrinsic Value per Share = (Sum of discounted FCFs + Discounted Terminal Value + Cash − Debt) ÷ Shares Outstanding

Each component is explained in the steps below.

Step 1: Find and normalize free cash flow

free cash flow (FCF) is the cash left over after the business has paid its operating expenses and invested in maintaining and growing its assets. It's the lifeblood of your valuation.

The simplest formula:

FCF ≈ Operating Cash Flow − Capital Expenditures

Find these figures on the cash flow statement. But don't just plug in last year's number blindly—normalize it first:

- Strip out one-time working capital movements that inflated or deflated the figure

- Check whether capex was unusually high (new factory build) or low (deferred maintenance)

- For cyclical businesses, use an average across a full economic cycle (typically 5–7 years)

Pro tip: If a company's reported FCF keeps mysteriously lagging net income year after year, management may be using aggressive accruals. Sustained FCF-to-net-income conversion below 80% is a yellow flag worth investigating.

Here's what a decade of FCF history looks like for a capital-light compounder—notice how consistently it converts earnings to cash:

Free cash flow trend

Cash left after funding operations and capital expenditure.

Operating cash flow

$81.3B

Capital expenditure

-$11.5B

Free cash flow

$69.8B

Step 2: Define your forecast horizon

Use 5 years for mature, slow-growth businesses where the future is reasonably predictable. Use 10 years for companies still in a compounding phase with durable competitive advantages.

Avoid going beyond 10 years of explicit forecasting. The further out you project, the less your estimates mean. Beyond year 10, you'll capture value through the terminal value instead.

Step 3: Model cash flow growth (in phases, not a straight line)

Most DCF guides tell you to pick one growth rate and apply it uniformly. That's a beginner mistake. Real businesses grow in phases.

A two-phase model is more realistic for most stocks:

- Phase 1 (Years 1–5): A higher near-term growth rate based on current business momentum, analyst consensus, or your own industry research

- Phase 2 (Years 6–10): A moderated rate as the business matures or competition increases

- Years 1–5: FCF grows at the Phase 1 rate, compounded annually from the base year

- Years 6–10: FCF grows at the Phase 2 rate, compounded from the Year 5 figure

Example: A software company with 15% near-term growth tapering to 8% in years 6–10 before reaching terminal growth.

Always ask: Is this growth rate consistent with the industry's total addressable market? Will reinvestment consume most of the cash flow? Growth without returns on invested capital (ROIC) above the cost of capital is value-destroying.

Step 4: Choose your discount rate

The discount rate is your required rate of return—the minimum annual return you demand to take on the uncertainty of owning this business.

For most retail investors, a simple personal hurdle rate works better than the academic WACC:

| Business Risk Profile | Suggested Discount Rate |

|---|---|

| Blue-chip, highly predictable (e.g., utilities) | 8–9% |

| Established compounders with moderate risk | 10–12% |

| Growth businesses with execution risk | 12–15% |

| Speculative or high-leverage situations | 15%+ |

Apply the discount factor to each year's FCF:

PV of FCF = FCF ÷ (1 + discount rate)^year

The counter-intuitive truth most investors miss: Your discount rate matters more than your growth rate. A 2-percentage-point change in the discount rate often swings intrinsic value by 20–30%. Investors spend hours debating whether a company will grow 10% or 12%, but barely question whether 10% is the right required return. Scrutinize your discount rate as carefully as you scrutinize growth.

Step 5: Calculate terminal value (and why it's the most dangerous input)

The terminal value (TV) captures all cash flows beyond your explicit forecast. In a 10-year DCF, it typically accounts for 60–75% of total enterprise value. That number should terrify you into conservatism.

The standard perpetuity growth model:

Terminal Value = (Final Year FCF × (1 + perpetual growth rate)) ÷ (discount rate − perpetual growth rate)

Where the perpetual growth rate is the long-run rate—capped at GDP growth, typically 2–3% in nominal terms.

Then discount the terminal value back to today:

PV of Terminal Value = Terminal Value ÷ (1 + discount rate)^years

Common mistake: Using a terminal growth rate of 5% or higher because the company "is still growing fast." Over a perpetual horizon, no company sustainably grows faster than the overall economy. Even Amazon or Apple eventually normalize. A 5% terminal growth rate vs. a 2.5% terminal growth rate can double your valuation output. That's a dangerous illusion of precision.

Step 6: Bridge from enterprise value to per-share intrinsic value

Your DCF produces an enterprise value—the value of the entire business regardless of how it's financed. To get to the equity value that belongs to shareholders:

Equity Value = Enterprise Value + Cash & Equivalents − Total Debt

Then divide by fully diluted shares outstanding (not basic shares—always use the diluted count, which includes options, RSUs, and convertibles):

Intrinsic Value per Share = Equity Value ÷ Diluted Shares Outstanding

Don't forget share count creep. If a tech company has been issuing 3% new shares annually to compensate employees, your per-share intrinsic value erodes every year even if enterprise value grows. Factor in expected future dilution.

Step 7: Apply a margin of safety

A DCF is not a fact—it's a structured guess. Even with careful research, you'll be wrong with some assumptions. The margin of safety is your buffer against that certainty.

Buy Price = Intrinsic Value × (1 − Margin of Safety %)

Conservative guidelines:

- 25% margin of safety for high-quality, predictable businesses

- 35–40% margin of safety for businesses with meaningful uncertainty or cyclicality

- 50%+ margin of safety for turnarounds, deep value, or capital-intensive situations

A stock trading at a 30% discount to intrinsic value isn't automatically a buy. First validate that your intrinsic value estimate is sound. The margin of safety protects against the gap between your model and reality—not against a bad model.

Here's what the margin of safety looks like in practice for a real stock:

Margin of safety

The gap between estimated intrinsic value and market price.

Current price

$317.31

Intrinsic value

$178.60

Margin of safety

-43.7%

Full worked example

Assumptions:

- Current normalized FCF: $1,000M

- Phase 1 growth (years 1–5): 10%

- Phase 2 growth (years 6–10): 6%

- Discount rate: 10%

- Terminal growth rate: 2.5%

- Net cash (cash minus debt): −$1,000M (net debt position)

- Diluted shares: 500M

FCF projections and present values:

| Year | FCF ($M) | PV Factor (10%) | PV of FCF ($M) |

|---|---|---|---|

| 1 | 1,100 | 0.909 | 1,000 |

| 2 | 1,210 | 0.826 | 999 |

| 3 | 1,331 | 0.751 | 1,000 |

| 4 | 1,464 | 0.683 | 1,000 |

| 5 | 1,611 | 0.621 | 1,000 |

| 6 | 1,707 | 0.564 | 963 |

| 7 | 1,810 | 0.513 | 929 |

| 8 | 1,918 | 0.467 | 896 |

| 9 | 2,033 | 0.424 | 862 |

| 10 | 2,155 | 0.386 | 832 |

- Sum of PV (FCF years 1–10): ~$9,481M

- Terminal Value at year 10: $2,155M × 1.025 / (0.10 − 0.025) = $29,418M

- PV of Terminal Value: $29,418M / (1.10)^10 = $11,349M

- Enterprise Value: $9,481M + $11,349M = $20,830M

- Equity Value: $20,830M − $1,000M (net debt) = $19,830M

- Intrinsic Value per Share: $19,830M / 500M = $39.66

- Buy Price at 25% MoS: $39.66 × 0.75 = $29.75

This is your anchor. Only buy if the market offers you the stock under $29.75.

Want to run these exact assumptions yourself and see how sensitive the output is to each input? Adjust the sliders below:

Present value calculation

How growth, discount rates, and terminal value shape a DCF.

- Starting FCF

- 100

- Forecast

- 10 years

- Growth rate

- 10%

- Discount rate

- 10%

Estimated present value

2,366.7

58% comes from terminal value

The scenario framework: stop using one set of assumptions

Every DCF you build is a single-point estimate. It creates false confidence. The fix is dead simple: always run three scenarios.

- Bear case: Lower growth (half your base case), slightly higher discount rate

- Base case: Your honest best estimate

- Bull case: Higher growth (1.5× base), stable discount rate

Then weight them:

Weighted IV = (25% × Bear case) + (50% × Base case) + (25% × Bull case)

If even the bear case suggests the stock is undervalued at the current price, your conviction level is justified. If you need the bull case to make the numbers work, that’s a speculation, not a value investment—and you should size accordingly. See how the three scenarios play out on a real company:

Valuation scenarios

A range is more honest than a single-point estimate.

$100.53

-68.3% vs. current price

$178.60

-43.7% vs. current price

$178.60

-43.7% vs. current price

The five intrinsic value calculation mistakes that cost investors money

- Forgetting that terminal growth compounds forever. A 4% terminal growth rate instead of 2.5% can inflate your valuation by 30–50%. Always cap at long-run GDP growth.

- Mixing cash flow types. Never discount net income or EBITDA in a DCF that is built for free cash flow. Each metric implies different assumptions about reinvestment.

- Using a too-low discount rate to justify a rich price. Lowering your required return from 10% to 8% to make a stock "look cheap" is reverse engineering—not analysis.

- Ignoring dilution. High share count growth destroys per-share value even when enterprise value compounds nicely.

- Building one scenario and calling it analysis. A single DCF without scenario testing is a comfort exercise, not a decision tool.

Frequently asked questions

Is intrinsic value the same as fair value?

The terms are often used interchangeably, but there's a subtle difference. Fair value sometimes implies a market-consensus estimate. Intrinsic value in the Buffett–Graham tradition means your independent, cash-flow-based estimate of what the business is worth to a rational long-term owner—independent of what the market currently says.

Do I need to use WACC as my discount rate?

Not for personal investing. WACC is a corporate finance concept that blends the cost of equity and debt. For a retail investor building a personal hurdle-rate DCF, using a single required return (e.g., 10–12%) is simpler and often more honest. WACC adds precision theater unless you have high confidence in your cost-of-equity and debt inputs.

What if the company has negative free cash flow?

You can still estimate intrinsic value, but you must model the timeline to cash flow breakeven and the capital needed to get there. That capital dilutes existing shareholders. Beginners should be cautious with negative-FCF companies until they are comfortable modeling multi-stage transitions.

How often should I update my intrinsic value estimate?

At minimum after each earnings report—quarterly for stocks you own or are watching. Any time the business fundamentals change materially (a major acquisition, a competitive threat, a margin structure shift), rerun your model with updated assumptions.

Stop guessing. Start measuring.

Most retail investors lose money not because they pick bad businesses, but because they buy at prices that already assume perfection. Learning to calculate intrinsic value gives you something rare: a rational anchor that is completely independent of market noise.

Build your model. Run your scenarios. Set your buy price. Then have the discipline to wait.

Apple Inc.

NASDAQ:AAPL

Intrinsic Alpha fair value

$178.60

Current market price

$317.31

Apple Inc.'s intrinsic value is $178.60, making it 43.7% overvalued relative to its current price of $317.31. This is Intrinsic Alpha's selected estimate based on the company's financial profile and available fundamentals.

Valuation runway

Price is 43.7% above intrinsic value

Current price

$317.31

If you're ready to run a real intrinsic value calculation on an actual company with live data—without building a spreadsheet from scratch—try the Intrinsic Alpha DCF Calculator. Adjust every assumption, run scenarios instantly, and see how sensitive the output is to each input.

The market will always offer you opportunities. The question is whether you'll be ready to act when it does.

About the author

Marcus Chen

Senior Writer

Marcus is a software engineer who turned a $30K portfolio into seven figures over 15 years of disciplined value investing. Entirely self-taught, he writes from experience, not theory, and lives by one rule: never buy what you can't value.